Jan 11 - Welcome to the home for real-time coverage of markets brought to you by Reuters reporters. You can share your thoughts with us at markets.research@thomsonreuters.com

RATE HIKING CYCLE PERKS (1215 GMT)

There's obviously a lot of angst surrounding the rate hiking cycle the Fed seems about to embark on in March but it's really not necessarily bad news for equities.

Register now for FREE unlimited access to Reuters.com

"An analysis of the last five hiking cycles by the Fed reveals that the S&P 500 rose every single time in the 12 months that followed the initial rate hike", writes Guilhem Savry, head of macro and dynamic allocation at Unigestion.

"On average, the index rose by 7.6% a year after the Fed first pulled the trigger", he adds, which might reassure those investors looking at the S&P 500's 2% drop since the beginning of the year.

Far from stagflation, the scenario Unigestion is considering moving forward isn't grim and involves "a gradual deceleration of growth and inflation, induced by easing supply constraints, which in turn should lessen the pressure on central banks to hike as aggressively as currently anticipated".

In terms of allocation, Unigestion points towards quality stocks and U.S. equities with a stronger dollar driving flows back into Wall Street.

Talking about flows, the mood is not very optimistic for British equities which are already within the tightening monetary cycle launched by the BoE.

"The problem for the UK market is that it remains firmly unpopular with global fund managers", IG analyst Chris Beauchamp noted this morning.

"Equity inflows have remained muted, and the monthly survey of active managers continues to point towards a general unwillingness to invest in UK stocks, a hangover perhaps of Brexit and the political uncertainty of 2019", he added.

While the FTSE 100 has pulled off a 50% jump since the lows of March 2020, it's still trading below its pre-pandemic highs despite its recent positive upward trend.

(Julien Ponthus)

*****

U.S. YIELDS: THE 2% THRESHOLD (1149 GMT)

U.S. rates are around levels not seen since March 2021 when they rose as high as 1.7% as optimism about the U.S. economy grew with the signing by President Joe Biden of the multi-trillion stimulus package.

But now analysts see a limited upside in yields as the terminal rate - or where central bank policy rates will peak - is expected to be lower than in the previous monetary tightening cycle of 2015-2018.

BofA agrees and recommends investors “to position for some consolidation near term” as it sees limited scope for “a further terminal re-pricing near term beyond 1.75%-2%.”

BofA’s “practical neutral rate (similar to terminal rate) may also be lower today (than in 2015-2018) because of a higher vulnerability of risk assets to interest rates.”

“We should expect rates to begin posing a material headwind to equities at a range of 1.75-2% 10-year,” BofA analysts say.

One other important factor in assessing the practical neutral rate “are the level of outstanding debt and the amount of debt servicing expense an economy can tolerate,” they add.

“We find that those peak 2018 debt loads would occur with 10y in a range of 1.5-2.5%, depending on how spreads change.”

So it seems that the big unknown is whether the Fed will be willing to become even more hawkish despite the risk of hurting the massive rise of prices in risky assets.

The chart shows the 10-year yield, around March 2021 levels, but way below the levels seen in 2018.

(Stefano Rebaudo)

*****

JUST A TECH GLITCH (0951 GMT)

As the upbeat market price action shows this morning, rising bond yields and higher interest rates don't necessarily mean 2022 is a lost cause for tech stocks.

As a matter of fact, many are the strategists who see the scare on tech stocks as just another opportunity to buy the dip.

"We view the recent equity volatility as an adjustment to the Fed’s incrementally more hawkish stance, rather than a sign that the Fed is about to bring the recovery and the equity rally abruptly to an end", UBS House View note read today.

"We still expect the rally to resume", the bank's strategists believe adding that cyclical sectors, financials and more widely, euro zone and Japanese equities, are expected to do well.

But there are other areas of tech which are seen promising too despite the upward direction of travel for yields.

"The areas of technology where we see most opportunity include artificial intelligence, big data, and cybersecurity", the UBS strategists also wrote.

Talking to us yesterday, Emmanuel Cau, head Of European equity strategy at Barclays also took the view that "the rise in real yields currently does not jeopardize equity markets".

Cau said he believes the rotation from tech to value is likely to continue but that doesn't mean that the whole tech sector should be avoided.

"The rise in yields will force the market to discriminate more between growth stocks and against the most vulnerable and speculative stocks which depended the most on abundant liquidity", he said.

Here's the European tech sector's performance in the past 5 years:

(Julien Ponthus)

*****

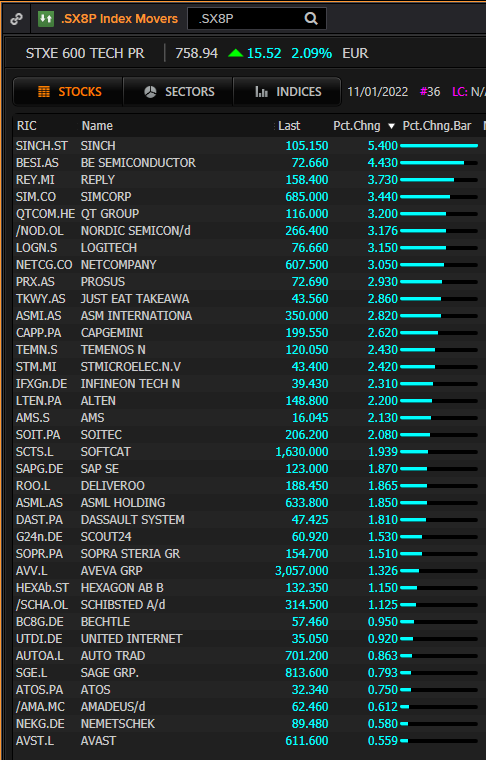

TECH STRIKES BACK! (0849 GMT)

Quite a spectacular rebound for European tech stocks this morning!

The sector's index is up well over 2% about 30 minutes after the opening bell, which suggests many traders believe yesterday's retreat was somewhat overdone.

As you can see below, there's not one single constituent of the tech index in the red:

The top performer in the sector is Sinch which is up 5% after Goldman initiated the stock with a buy recommendation which suggests a 45% upside.

While it's not in the index, shares of British cybersecurity firm Darktrace are jumping over 17% after an upbeat revenue outlook.

Another growth company, Delivery Hero, is also shining at the top of the STOXX 600 with a 5% rise.

The pan-European equity benchmark is up 0.7%.

All in all, it seems the rise in bond yields might not be just as detrimental than what investors foresaw on Monday.

Quite logically, with the angst on rising yields easing, the banking sector is among the few losers this morning with a 0.25% drop.

Banking shares are still up close to 7% so far in 2022.

(Julien Ponthus)

*****

WHERE WILL IT END? (0820 GMT)

Did retail investors save the day? The Nasdaq, which fell more than 2% at one point on Monday managed to close in positive territory, as bargain hunters swept in.

It's a scenario seen repeatedly in the past year and often attributed to amateur traders. Buy buyside analysts were also out in force with buy-the-dip advice, noting that markets were well on their way to pricing the likelihood of four U.S. rate hikes this year, making further hawkish surprises harder.

Possibly, that's kept the dollar flatlining this month, well off 16-month highs touched at the end of November, while Treasury yields on Monday snapped a six-session rising streak.

As we write, Wall Street futures appear undecided on direction though European shares are opening firmer. Bar any fresh news, markets will likely wait to see if Wednesday's U.S. consumer inflation print indeed breaches 7%, as anticipated.

In a reminder of global inflation pressures, a survey showed Japanese households' inflation expectations at a more than two-year high. read more

Policymakers seem calmly confident though they can avert runaway inflation; pre-released comments show Federal Reserve Chair Jerome Powell will tell Congress the bank would "prevent higher inflation from becoming entrenched" read more .

And while euro area inflation is running at 5%, ECB chief economist Philip Lane says he does not see prices above the 2% target in the medium term .

Markets for now remain convinced that the interest rate peak, the so-called terminal rate, will be lower than in previous cycles.

Goldman Sachs is among those warning that U.S. terminal rate pricing is too low. But with the Nasdaq market cap down more than 4% this year, it may be bargain-hunting time.

Key developments that should provide more direction to markets on Tuesday:

-"Grand Theft Auto" video game maker Take-Two Interactive to buy Zynga for $11 billion read more

-Britons splurged on eating at home pre-Xmas, shunned restaurants read more

-ECB President Christine Lagarde to speak

-Fed speakers: Chairman Jerome Powell; Kansas City President Esther George

-U.S. 3-year note auction

(Sujata Rao)

*****

DIP-BUYING TUESDAY? (0712 GMT)

European shares look set for some kind of a rebound this morning as rising futures for the main benchmarks show investors are ready to buy at least some of yesterday's dip.

On that note, Marko Kolanovic, chief global markets strategist at JPMorgan wrote yesterday that Wall Street's recent sell-off presents a buying opportunity. read more

Euro STOXX 50, DAX, FTSE and IBEX futures are up between 0.1% and 0.4% but on Wall Street, futures are still slightly in the red.

Rising yields are indeed keeping the pressure on equity markets and investors still very much focused on Wednesday's U.S. inflation data with the headline CPI seen climbing to 7% year-on-year.

(Julien Ponthus)

*****

Register now for FREE unlimited access to Reuters.com

Our Standards: The Thomson Reuters Trust Principles.

"cycle" - Google News

January 11, 2022 at 07:16PM

https://ift.tt/34uTCf0

LIVE MARKETS Rate hiking cycle perks - Reuters

"cycle" - Google News

https://ift.tt/32MWqxP

https://ift.tt/3b0YXrX

Bagikan Berita Ini

0 Response to "LIVE MARKETS Rate hiking cycle perks - Reuters"

Post a Comment