Jan 31 - Welcome to the home for real-time coverage of markets brought to you by Reuters reporters. You can share your thoughts with us at markets.research@thomsonreuters.com

TIGHTENING CYCLE: NO ALARMS AND NO SURPRISES PLEASE (1130 GMT)

Looking at Wall Street's close and European equity markets this morning, it does seem like investors have made their peace with the tightening cycle going ahead at a faster pace than initially foreseen.

Register now for FREE unlimited access to Reuters.com

"The consensus view was that the recent equity market correction is probably overdone in the near term", wrote Ben Bennett, head of investment strategy at LGIM.

As noted by Neil Wilson at Markets.com, "tantrums are usually on the threat, not on the deed: market knows the Fed is tightening swiftly this year and possibly every meeting".

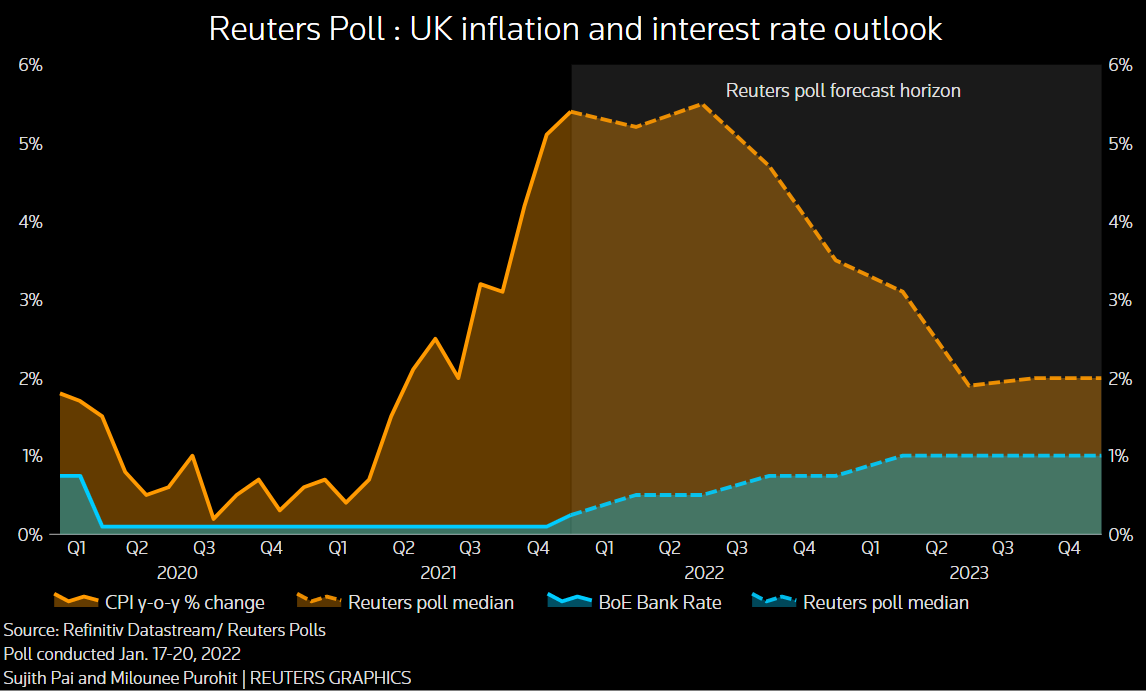

Knowing what to expect, investors are unlikely to go on a selling frenzy if the pace of hikes meets the expected direction of travel, for instance with the BoE raising rates at its meeting this week.

"This is widely expected by the market and unlikely to prompt any volatility among UK stocks unless the central bank is aggressive with the amount by which it puts up rates", argued Russ Mould at AJ Bell.

But there is still room for surprises on that front with the reduction in the balance sheet adding a layer of complexity.

RBC strategist Adam Cole the interaction between rate hikes and balance sheet reduction "means this will not be a ‘normal’ tightening cycle and that current pricing for Bank Rate is too aggressive".

And there are actually many more unknowns when it comes to other central banks.

A 50 basis point hike by the Fed in March definitely seems a possibility, like Raphael Bostic told the FT. That prompted Natwest Markets to warn markets not to rule that possibility out.

Consensus is for between four and five rate hikes in 2022 but Berenberg economists now expect six rate hikes in 2022, four further in 2023 and one 2024.

And while the ECB's wise owl Christine Lagarde explicitly said that a rate hike this year very unlikely, investors have priced in some 20 basis points of hikes before 2023. Deutsche Bank expects a 25 basis point rate liftoff in December 2022.

In a nutshell, there's definitely room for alarms and surprises in this tightening cycle.

Some reading:

Bank of England to raise rates again in February as inflation surges read more

ANALYSIS-'Nimble' Fed narrows normalisation window for timid ECB read more

Fed rate hike could be half-point if needed, says Raphael Bostic -FT read more

(Julien Ponthus)

*****

BUY SIGNALS (1002 GMT)

It's been a bruising month for risk assets but a range of technical indicators say it's time for investors to jump back in, even though geopolitical and rate jitters are here to stay.

JP Morgan says its Vix signal entered "buy territory" last week, a move which historically has been a prelude to stock market gains over the following 1-6 months in 100% of the times outside recessions.

Also, according to strategists at the U.S. investment bank, equities have plunged to oversold levels and the market internals are "encouragingly staying pro-risk"..

"We continue to believe that one should be using the dips as the opportunities to add, and favour Cyclicals, Banks, Commodities, against Defensives such as Healthcare, and Tech," they conclude.

Some earlier reading on buy signals: GRAPHIC-Market signals scream buy after world stocks tumble read more

(Danilo Masoni)

*****

STOXX ON THE UP, ITALY OUTPERFORMS, TECH LEADS (0903 GMT)

Equities in Europe kicked off another big week for central bank meetings on the right foot with the STOXX 600 rising over 1% in early deals helped by Wall Street's late bounce on Friday.

Italian stocks stood out, up 1.6% after the re-election of outgoing President Mattarella averted a political crisis, offering relief to investors and boosting local banking stocks (.FTITLMS3010), as the country-s borrowing costs fell.

Tech (.SX8P) was the biggest gainer, up 2.8% from an 8-month low, while travel and leisure (.SXTP) lagged after Ryanair reported a Q4 loss but said it was hopeful that rivals' cuts to capacity may help push prices up in the summer season.

Profit warnings at oil services firm Saipem and French retailer Casino added some gloom, sending their shares down as much as 27% and 9% respectively.

(Danilo Masoni)

******

WALK ON THE WILD SIDE (0743 GMT)

The days of wild swings aren't over. And with bears and bulls still fiercely wrestling for control, investors could see their nerves tested again this week as geopolitical tensions build up and policy tightening remains centre stage.

So while the Bank of England is set to raise rates for the second time in a row and the Fed's Bostic said a supersized rate hike may be needed, the U.K. warned it was "highly likely" that Russia was looking to invade Ukraine and NATO voiced concern over Europe's energy security.

And if it weren't enough, North Korea tested an intermediate-range nuclear-capable missile for the first time since 2017. The U.S. said the test was part of an "increasingly destabilizing" pattern and urged Pyongyang to join direct talks.

With Chinese markets closed, European stock futures were up 1.5% ahead of the cash market open, powered by Friday's late rally on Wall Street to its best day this year following a frantic week of topsy-turvy trading.

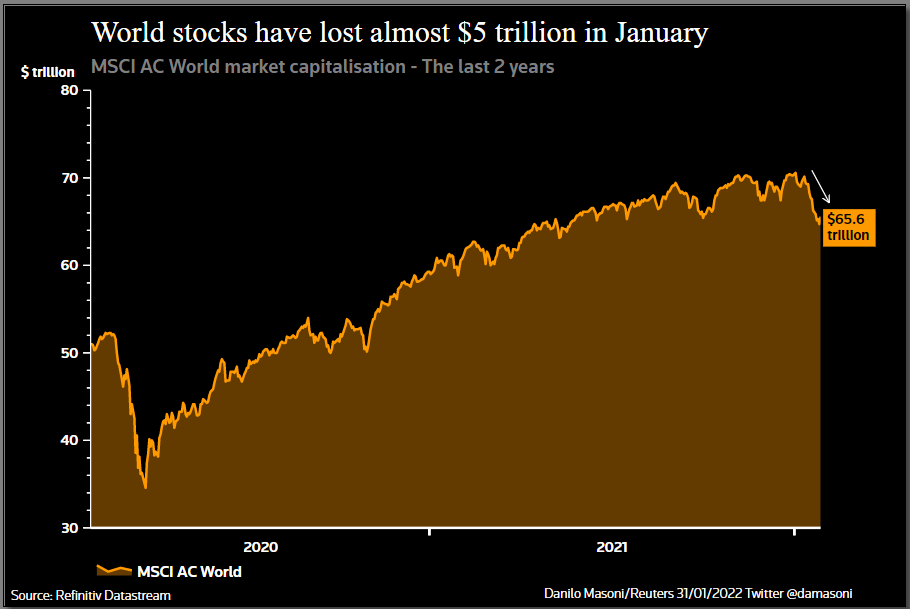

World shares (.MIWD00000PUS) have erased nearly $5 trillion of market cap this year and are set for their worst month since April 2020, in a downtrend partly cushioned by positive soundings from the earning season.

Weekend political events also brought some relief.

The re-election of outgoing 80-year-old Italian President Mattarella means former ECB boss Draghi will carry on as prime minister. And in Portugal the Socialists won an outright parliamentary majority in a snap election, defying all odds.

As a result, Italy's 10-year bond yields saw a chunky drop of over 6 basis points, narrowing the spread against the safer German equivalent .

Key developments that should provide more direction to markets on Monday:

- Goldman Sachs ups forecasts on U.S. Federal Reserve rate hikes to five times in 2022 from four earlier

- Japan's factory output shrank for the first time in three months in December

- Growth in China's factory activity slowed in January as a resurgence of COVID-19 cases and tough lockdowns hit production and demand, but the slight expansion offered some signs of resilience

- Ryanair reported a loss of 96 million euros for the final three months of 2021 but said it was hopeful that rivals' cuts to capacity may help push prices up in the key summer season

- Shares of Macau Legend, which owns and operates a casino resort in Macau, fell more than 20% to an all-time low on Monday after its chief executive was arrested and detained by police in the world's largest gambling hub

- German Q4 flash GDP/prelim CPI and HICP

- Fed speakers: San Francisco Fed President Mary Daly; Kansas City President Esther George

- Chicago PMI

- European earnings: Evraz, Ryanair, Siemens Healthineers

(Danilo Masoni)

*****

Register now for FREE unlimited access to Reuters.com

Our Standards: The Thomson Reuters Trust Principles.

"cycle" - Google News

January 31, 2022 at 06:31PM

https://ift.tt/nuoXHmOkB

LIVE MARKETS Tightening cycle: no alarms and no surprises please - Reuters

"cycle" - Google News

https://ift.tt/6YAiCyUof

https://ift.tt/53eFYlmiP

Bagikan Berita Ini

0 Response to "LIVE MARKETS Tightening cycle: no alarms and no surprises please - Reuters"

Post a Comment